Weekly Reads

A space where we share a selection of thought-provoking content that we've recently come across.

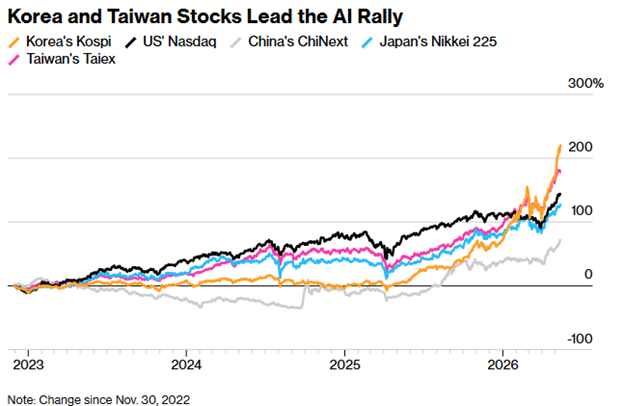

World’s biggest stockrally ignites speculative mania in Korea

SouthKorea’s Kospi has surged more than 200% over the past year, cementing itsposition as the world’s best-performing major equity market by a wide margin.The catalyst is clear: Samsung Electronics and SK Hynix sit at the center ofglobal AI infrastructure, supplying the high-bandwidth memory that hyperscalerscannot build without — Samsung alone posted a 755% increase in profit in Q1.But the rally has attracted a second wave of participants with a differentdisposition. Retail margin debt has hit unprecedented levels, daily 5%+ priceswings have become routine, and one local observer captured the mood: “there isa growing sentiment that social mobility is no longer possible throughtraditional means — it is only achievable through speculative assets.” Anotherwas blunter: “People with FOMO see others making big profits and may jump inrecklessly, often using excessive leverage. But no one knows when the bull runwill end.” Meanwhile, foreign institutions were net sellers of $11.5 billion inMay alone. The divergence between who is buying and who is selling is a dynamicthat historically resolves in one direction.

Amazon staff use AI tool for unnecessary tasks to inflate usage scores

Amazonrecently rolled out an internal AI agent platform called MeshClaw, which allowsemployees to create agents that can initiate code deployments, triage emails,and interact with Slack on their behalf. The tool was designed to accelerateproductivity. What it has produced, at least in part, is a new category oforganizational behavior: employees running unnecessary AI tasks purely toinflate their token consumption scores on internal leaderboards. Amazon settargets for more than 80% of its developers to use AI weekly and tracked usagein dashboards. The company told staff the statistics would not be used inperformance evaluations, but multiple employees told the FT they believedmanagers were monitoring the data regardless—creating what some described as“perverse incentives.” Other people said “there is just so much pressure to usethese tools,” and “some people are just using MeshClaw to maximize their tokenusage.” The phenomenon has acquired a name: “tokenmaxxing.” It is anear-perfect illustration of Goodhart’s Law—when a measure becomes a target, itceases to be a good measure.

KrishnaRao, Anthropic’s CFO, makes his first public appearance in a conversation thatcuts to the economics of the frontier AI race. Anthropic’s thesis is that thereturns to frontier intelligence are extremely high and not slowing down. Everynew model generation unlocks a wider TAM that enterprise customers immediatelymonetize. This thesis is backed up by the fact that Anthropic’s annualized runrate (ARR) began the year at $9bn and has increased to $45bn as of May 2026. Netdollar retention exceeds 500%. The risk that keeps Rao up at night is compute.Anthropic has committed over $100bn across Google TPUs, AWS Trainium, andNvidia GPUs. Buy too much and the business fails, buy too little and you losethe frontier race.

Former Apollo risk chiefsays some new life insurers could struggle in downturn

Chak Raghunathan, former chief risk officer at Apollo Management and now an adviserto firms including Josh Harris’ 26North and Brookfield’s AEL, is sounding analarm that deserves more attention than it is getting. His concern isstructural: a generation of Wall Street-backed life insurers have quietlyloaded their balance sheets with untested private credit while simultaneouslyselling newer savings products—principally annuities—that are more vulnerableto withdrawals than traditional policies. In a downturn, those two featuresinteract badly. Deteriorating private credit marks create policyholder anxiety;anxious policyholders surrender annuities; surrenders force asset sales into anilliquid market; asset sales further impair marks. The potential doom loop isnot hypothetical—it mirrors the logic of every prior liquidity crisis ininsurance, just with a new asset class at its center. Raghunathan’s credentialmatters here: he built Apollo’s risk management framework from 2008 to 2014 andhas since advised insurers on both sides of this trade. His verdict is blunt:“Some of these guys, in my opinion, are going to be in trouble.” The USTreasury held meetings with state insurance commissioners on exactly this topiclast week.

Meta VP of Monetization InfrastructureMatt Steiner on ads, chips, and AI foundations

Meta'sCFO Susan Li flagged during their Q1 2026 earnings call that the company hadmade an architectural change to how it ranks ads: a new adaptive ranking modelthat improves inference ROI by routing requests to more compute-intensivemodels when the probability of conversion is higher. Matt Steiner, Meta's VP ofMonetization Infrastructure, Ranking, and AI Foundations, sits down with AustinLyons on his Chipstrat podcast to explain the infrastructure logic behind it.The core insight is that recommender workloads are fundamentally different fromLLM workloads — they are memory-bound rather than compute-bound — which is whystandard GPU architectures are the wrong tool and why Meta's MTIA customsilicon program exists in the first place. The more surprising thread is whatMeta calls KernelEvolve: a program that uses LLMs to write optimized kernelsfor its heterogeneous chip fleet. As kernel generation approaches zero marginalcost, Meta is targeting roughly 100x more optimized kernels per chip than it currentlyhas, turning software optimization from a human bottleneck into an automatedcompounding flywheel. The conversation is technical, but the business logicunderneath is not: at Meta's scale, every percentage point of inferenceefficiency converts directly into margin.